.webp)

If you've missed a few EMIs and started searching for the best loan settlement app in India, you've probably noticed something: every app claims to be the best. That makes the search harder, not easier. Here's a more useful way to evaluate your options what a legitimate settlement app should actually offer, how the process works, and which red flags mean you should walk away immediately.

What Loan Settlement Actually Is

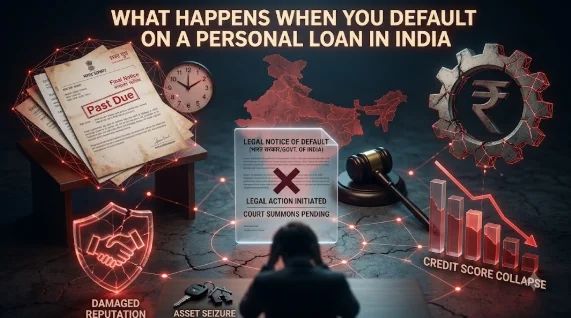

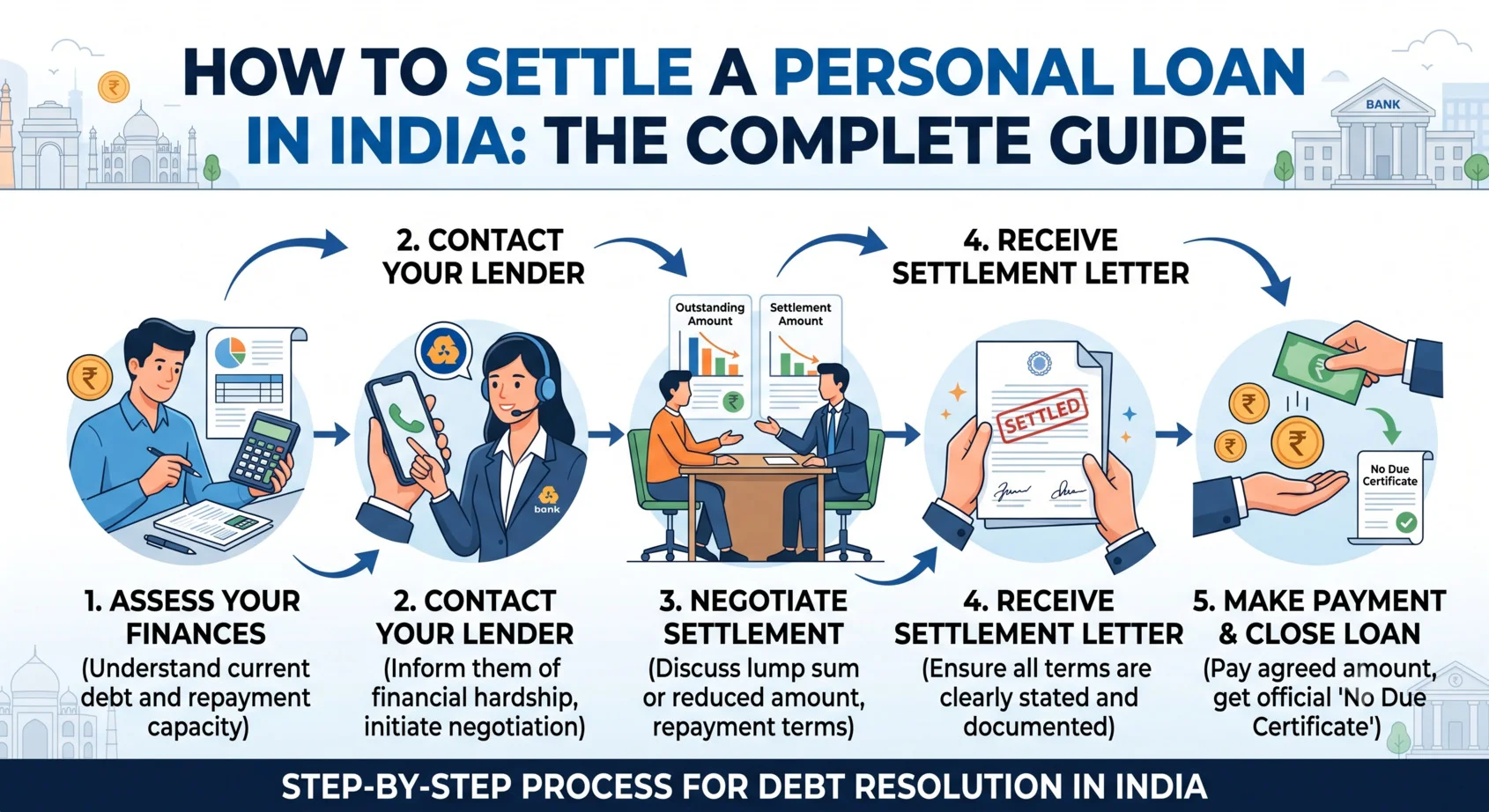

Loan settlement means negotiating with your lender to close a loan for less than the full outstanding amount including accrued interest and penalties through a single reduced payment. The lender agrees to this because recovering something is better than recovering nothing from a borrower who genuinely can't repay in full.

It's a legitimate, RBI-recognized process (usually called a One-Time Settlement, or OTS), not a loophole or a scheme. But it's meant for people in genuine hardship job loss, medical emergencies, income disruption not as a way to skip payments you can actually afford.

Why So Many People Are Searching for This Right Now

A few patterns show up repeatedly among borrowers looking into settlement apps:

- Income shocks - a layoff or pay cut that made previously manageable EMIs unaffordable overnight

- Medical emergencies - hospital costs that ate into the money meant for loan repayment

- Loan stacking - multiple EMIs across personal loans, credit cards, and BNPL that quietly became unmanageable

- Business slowdown - self-employed borrowers hit by a drop in income

If any of this sounds familiar, you're not in an unusual situation this is one of the most common financial spirals in India right now, and it's exactly what settlement tools exist to address.

What to Actually Look For in a Settlement App

Not every app that advertises "loan settlement help" delivers it responsibly. Before trusting any platform with your financial details, check for these:

1. Direct lender connection - the app should put you in touch with your actual lender, not route you through unnecessary middlemen who add fees and delays.

2. No upfront fees - a trustworthy platform charges only after a settlement is successfully closed, never before.

3. A track record you can verify - look for app store ratings, review volume, and any published success data, and treat it as a claim to verify rather than a guarantee.

4. Coverage across loan types - personal loans, credit card dues, NBFC loans, and business loans, not just one narrow category.

5. A transparent process - you should see every offer and document before agreeing to anything, with no surprise charges.

6. Support with collection pressure - a decent platform should help reduce harassment from recovery agents during the process, not just leave you to handle it.

7. Post-settlement credit rebuilding guidance - settlement affects your CIBIL profile, so ongoing support after closure matters as much as the negotiation itself.

Comparing the Three Ways to Settle a Loan in India

Option 1: Go direct to your bank. You can request an OTS yourself. No fees involved, but you're negotiating against people who do this professionally every day, and most borrowers end up with a worse deal than they could have gotten with guidance.

Option 2: Hire a third-party settlement agent. Common, but risky many charge 5–15% of the settled amount, often upfront, and there's a real fraud problem in this space. If anyone asks for cash before a settlement is confirmed, that's a hard stop.

Option 3: Use a dedicated settlement app. This is where platforms like Zavo try to combine direct lender access with structured guidance the idea being you get the negotiating leverage of going straight to the bank, without doing it blind. Zavo states it charges only on successful settlement and reports a 97% success rate across more than 10 lakh users, though as with any such figure, it's worth treating as the platform's own claim and checking current app store reviews for a live read on user experience.

Settlement vs. EMI Relief Not the Same Thing

These get mixed up constantly:

EMI relief is a temporary adjustment - reduced EMI, a moratorium, or restructured repayment. Your total debt stays roughly the same; you're buying time, not reducing what you owe.

Loan settlement closes the debt entirely for less than the original amount, typically once repayment has become genuinely impossible.

If you can still manage payments with some breathing room, relief may be the better first step. If repayment in full is off the table, settlement is the more relevant conversation.

Who Settlement Actually Makes Sense For

This route tends to fit if:

- You've missed three or more EMIs and the account is in default

- You've tried negotiating with the lender directly and hit a wall

- Collection calls have become a daily occurrence

- You can manage a one-time reduced payment, even if full repayment isn't possible

- You want a defined end point rather than an open-ended default sitting on your file

Fraud Patterns to Watch For

A few red flags come up repeatedly with predatory "settlement" schemes:

- Requests for cash payment upfront, before anything is confirmed

- WhatsApp groups promising blanket loan waivers

- Messages claiming to be an official "RBI settlement scheme"

- Any app or agent asking for your net banking login or OTP

No legitimate lender or settlement platform will ever ask for your banking credentials directly.

The Bottom Line

There's no single universally "best" loan settlement app what matters is whether a platform is transparent about fees, gives you direct lender access, and supports you after settlement, not just during it. Whichever platform you choose, verify claims independently check current app store ratings, read recent reviews, and confirm RBI-compliant practices rather than taking success-rate numbers at face value. Platforms like Zavo are worth evaluating against this checklist alongside a couple of alternatives before deciding.Frequently Asked QuestionsIs loan settlement legal in India?

Frequently Asked Questions

Q1 - Is loan settlement legal in India?

Yes. One-Time Settlement is a recognized, lender-approved process for closing a loan below the full outstanding amount when a borrower genuinely cannot repay in full.

Q2 - Will using a settlement app affect my credit score?

The app itself doesn't affect your score the settlement outcome recorded by your lender does. A "Settled" status is generally viewed less favorably than "Closed" and stays on your report for a period, though it's typically less damaging long-term than an unresolved default.

Q3 - Can I settle credit card debt through these apps, or only personal loans?

Most full-service settlement apps cover personal loans, credit card outstanding balances, and NBFC dues under one process worth confirming for any specific platform before signing up.

Q4 - Do collection calls stop immediately once I start the process?

Not immediately, but pressure typically eases once a formal settlement process is underway, since the lender is aware a resolution is in motion.