.webp)

I still remember the moment my colleague Priya broke down in the office cafeteria. She had been managing three credit cards, juggling minimum payments, and taking small personal loans just to keep her head above water. By the time she came to me for advice, her total credit card debt had crossed ₹3.8 lakhs, and she hadn't slept properly in weeks.

What she needed wasn't more advice about budgeting. She needed a real solution. That solution turned out to be credit card settlement.

If you're reading this right now, there's a good chance you or someone you know is in a similar situation. Maybe the numbers on your credit card statement keep growing despite your best efforts. Maybe you've started avoiding calls from unknown numbers. Maybe you're wondering if there's any way out that doesn't involve selling your assets or borrowing from relatives.

This guide is written for you. No jargon. No judgment. Just real, practical information about how credit card settlement works in India in 2026.

Let's Start With the Basics: What Is Credit Card Settlement?

Credit card settlement is a formal agreement between you and your credit card issuer where you pay a reduced amount to close your outstanding debt permanently.

Here's a simple way to understand it.

Say you owe ₹2,50,000 on your credit card after accumulated interest, late fees, and penalties. If you're genuinely unable to pay this full amount, you can approach the bank and negotiate. After back and forth discussions, the bank might agree to accept ₹1,20,000 as full and final payment. The remaining ₹1,30,000 gets written off.

Once you make that payment and receive the No Dues Certificate, your obligation to that bank for that credit card account is over.

That's credit card settlement in its simplest form.

Why Would a Bank Agree to Take Less Money?

This is the question most people ask first. And it's a fair one.

Banks are not charities. They exist to make money. So why would HDFC Bank or ICICI Bank or SBI Card agree to settle for 50 paise on the rupee?

The answer comes down to practical risk management.

When a borrower stops paying for 90 days or more, the account gets classified as a Non-Performing Asset (NPA) internally. The bank knows at this point that recovering the full amount is uncertain. They have two choices:

Option A: Spend months or years pursuing legal action, hiring collection agencies, and dealing with court proceedings. This costs money and time. Even if they win, executing the judgment against someone with no assets is nearly impossible.

Option B: Negotiate a settlement, recover a significant portion of the money quickly, and close the file.

Most banks, especially for amounts under ₹5-10 lakhs, prefer Option B. It's cleaner, faster, and more economical.

That's why settlement is a realistic possibility for ordinary borrowers. The bank genuinely needs to find a middle ground sometimes.

Who Should Consider Credit Card Settlement?

Let me be very clear about this because it matters.

Credit card settlement is not a hack to avoid paying your dues. It is a debt resolution option for people who are genuinely in financial distress.

You should consider it if:

- Your outstanding credit card debt is more than six months of your take-home salary

- You have been unable to pay even the minimum amount due for three months or more

- You've faced a genuine hardship like job loss, medical emergency, business failure, or divorce

- Your interest and penalty charges are growing faster than you can pay them down

- Collection agents are calling you regularly and the mental stress is affecting your health and work

- You have no significant assets that could be liquidated to pay the debt

If you can afford to pay but simply don't want to, settlement is not the right path. It will damage your credit score and create complications that will follow you for years.

But if you're genuinely stuck, settlement might be the most sensible financial decision you can make in 2026.

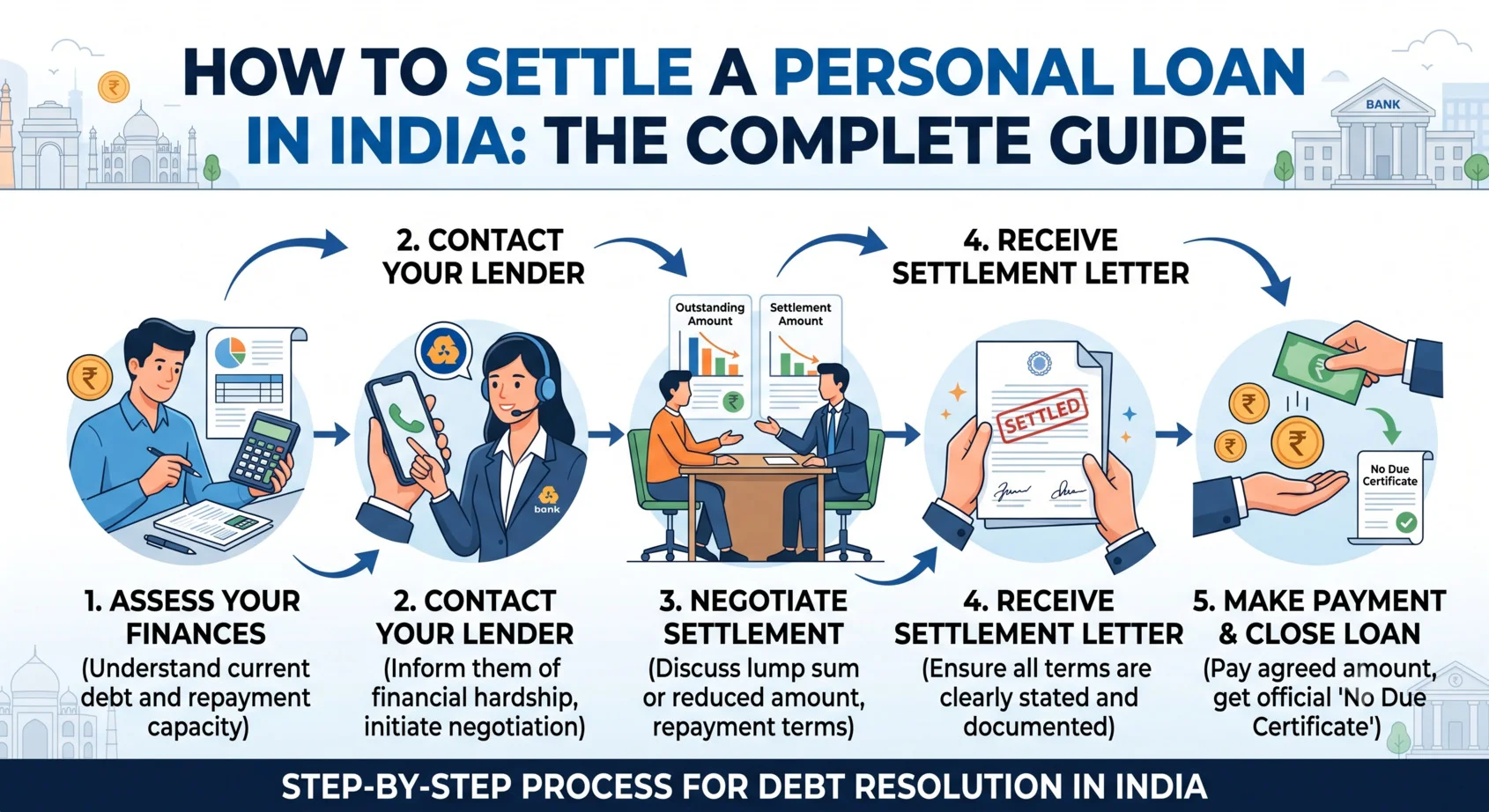

The Complete Credit Card Settlement Process in India

Let me walk you through exactly how this works from beginning to end.

Phase 1: Recognizing the Situation

Before anything else, you need to sit down and honestly assess where you stand. This means:

- Adding up your total outstanding balance across all credit cards

- Calculating how much you realistically owe after interest and penalties

- Understanding your current monthly income and essential expenses

- Determining what lump sum amount you could genuinely arrange if required

This clarity is important before you approach any bank. You need to know your numbers.

Phase 2: Allowing the Account to Age

This is the uncomfortable part that many people don't tell you about upfront.

Banks will not seriously discuss settlement with a borrower who is actively making payments, even minimum payments. The moment you keep paying, they have no real incentive to negotiate.

For settlement to become viable, your account typically needs to be overdue for at least 60 to 90 days. Some banks wait until 120 to 180 days before becoming genuinely open to discussion.

This means you will need to stop paying for a period. Yes, this will hurt your credit score and generate collection calls. But if you were already heading toward default, this step makes the overall outcome better, not worse.

Phase 3: Opening Negotiation

Once your account is sufficiently overdue, you initiate contact. You can either reach out proactively to the bank's customer service or collection department, or respond to their collection calls with a settlement proposal.

Your opening offer should be conservative. Start by offering 25 to 35 percent of the total outstanding amount. The bank will almost certainly counter higher, but starting low gives you room to negotiate.

During this conversation, always present your financial hardship clearly and honestly. The more the bank understands your genuine inability to pay the full amount, the more flexible they tend to become.

Phase 4: The Back and Forth

Negotiation rarely settles in one call. Expect multiple conversations over several days or even weeks.

Based on experience and current trends in India, most settlements land between 40 percent and 65 percent of the outstanding amount. Individual bank policies, the specific account history, and your negotiation skills all influence the final number.

Keep notes of every conversation. Note the date, time, name of the representative, and what was discussed.

Phase 5: Getting It in Writing

This step is non-negotiable. Absolutely nothing gets paid without a written settlement letter.

The letter must include:

- Your full name and credit card account number

- The total outstanding amount as of the settlement date

- The agreed settlement amount

- A clear statement that this payment constitutes full and final settlement

- The payment deadline

- The bank's commitment to issue a No Dues Certificate after payment

- Authorized signature from the bank

If any bank representative pushes you to pay first and promises to send the letter later, decline. This is a common situation that leads to disputes. Payment comes only after documentation.

Phase 6: Making the Payment

Transfer the settlement amount through a documented channel. Bank transfer, demand draft, or NEFT are preferred over cash. Always keep your payment receipt.

Phase 7: Collecting Your No Dues Certificate

After payment clears, follow up immediately for your No Dues Certificate. This document confirms your account is closed and no further dues exist. Store it safely because you may need it in the future if there are any disputes.

How Credit Card Settlement Affects Your CIBIL Score

Let's talk honestly about the credit score impact because many people get a shock after settlement.

When you settle a credit card debt for less than the full amount, credit bureaus like CIBIL mark the account as "Settled" in your credit report. This status is different from "Closed" which appears when you repay in full.

A "Settled" status signals to future lenders that you didn't repay the full amount you borrowed. As a result:

- Your CIBIL score typically drops by 75 to 150 points depending on where it was before

- The settled status remains on your credit report for seven years

- Getting new credit cards or loans becomes harder during this period

- Home loans and large personal loans in particular may be difficult to obtain

However, here's the perspective that matters.

If you're already defaulting on payments for several months, your credit score is already falling. The question isn't whether settlement hurts your credit. The question is whether settlement or continued default hurts it more.

Prolonged default with no resolution is worse for your long-term financial health than a settlement that at least closes the chapter and lets you start rebuilding.

After settlement, you can gradually rebuild your credit score over two to three years through responsible financial behavior.

Settlement Amount: What Percentage Can You Expect?

This varies considerably based on several factors.

Factors that improve your settlement percentage (you pay less):

- Longer period of default (banks become more flexible the older the debt is)

- Genuine documented financial hardship

- Smaller outstanding amount

- No significant assets in your name

- Willingness to pay the settled amount as a lump sum quickly

Factors that work against you:

- Recent default (just a month or two)

- Stable income or visible assets

- No clear reason for financial difficulty

- Requesting payment in installments rather than lump sum

As a rough guide for 2026:

These are general estimates. Your actual settlement will depend on the specific bank, your account history, and how you negotiate.

DIY Settlement vs. Professional Debt Resolution Services

You have two paths here and both have merit depending on your situation.

Handling It Yourself

If you're comfortable with phone negotiations, can stay calm under pressure, and have the time to manage the process, you can handle settlement yourself.

The advantage is that you pay no service fees. The disadvantage is that bank representatives deal with these conversations daily while you may be doing it for the first time. This experience gap can cost you money if you settle at a higher percentage than a professional would have achieved.

Working With a Debt Resolution Company

Professional services like The Zavo specialize specifically in

credit card settlement in India. They bring several real advantages:

- They know the negotiation benchmarks for each major bank

- They handle all communication so you don't have to deal with collection calls

- They understand the documentation requirements to protect you legally

- They often negotiate settlements that are meaningfully lower than what individuals achieve on their own

- They provide structured guidance through every step

Their fees are typically a percentage of the settled amount or a fixed fee structure. Even after fees, many people end up paying less overall than they would have settling on their own, simply because of better negotiation outcomes.

If the thought of negotiating directly with banks feels overwhelming, or if you have multiple credit cards to settle simultaneously, professional help is worth seriously considering.

What the Law Says About Credit Card Settlement in India

A few important legal points that every borrower should understand.

It's completely legal: Credit card settlement is a recognized and legal debt resolution mechanism. There's nothing improper about negotiating with your lender.

RBI guidelines protect you: The Reserve Bank of India has clear guidelines on fair debt collection practices. Banks and collection agencies cannot threaten you, visit your home or workplace repeatedly without notice, use abusive language, or contact your family members. If any of this happens, you can file a complaint with the RBI or Banking Ombudsman.

Statute of limitations: In India, the limitation period for recovering a debt is typically three years from the date of default. After this period, a bank cannot legally sue you to recover the debt, though they can still pursue it through other means. This doesn't mean you should ignore old debt, but it's important context.

Written agreements are binding: A written settlement letter signed by an authorized bank representative is a legally binding document. Once you pay per the terms and they issue the NDC, the matter is settled in the eyes of the law.

Tax Considerations You Cannot Ignore

Here's something most settlement guides skip over that can catch people off guard.

Under Indian income tax law, if a lender waives off more than ₹50,000 of your debt, the waived amount may be considered as income in your hands. This falls under "income from other sources" in your ITR filing.

For example, if your outstanding was ₹2,00,000 and you settled for ₹90,000, the bank wrote off ₹1,10,000. This forgiven amount might need to be declared as income and could attract tax liability depending on your overall income slab.

This is not always enforced uniformly and depends on individual circumstances. However, it's important to speak with a CA or tax consultant before and after settlement to understand your specific tax obligations. Being surprised by a tax notice months after settlement is the last thing you need.

Common Mistakes That Cost People Dearly

Over time, certain mistakes come up repeatedly in credit card settlement situations. Knowing these in advance can save you significant money and stress.

Paying before getting written confirmationAlways receive the settlement letter before transferring any money. No exceptions.

Accepting a verbal settlement offerA phone call or verbal assurance means nothing legally. Insist on written documentation.

Failing to negotiate the starting offerThe bank's first offer is never their best offer. Always counter lower and negotiate from there.

Not keeping copies of everythingEmails, letters, payment receipts, NDC — keep copies of all of these in both digital and physical formats.

Rushing into settlement without exploring alternativesSometimes a balance transfer, debt consolidation loan, or EMI restructuring might work better for your situation. Explore all options before committing to settlement.

Ignoring the tax implicationsAs mentioned above, speak to a tax professional about the forgiven amount.

Taking on new credit immediately after settlementGive yourself at least 12 to 18 months to stabilize your finances before taking on new credit obligations.

Alternatives Worth Considering Before Settlement

Settlement should not be your first response to credit card stress. Consider these alternatives first.

EMI Conversion: Most banks allow you to convert your outstanding balance into a structured EMI at a lower interest rate. If you have income but struggle with the revolving balance, this might be enough.

Hardship Programs: Some banks have internal programs for customers facing genuine difficulty. These might offer temporary payment pauses or reduced interest for a period.

Balance Transfer: Moving your balance to a card with a lower interest rate or a zero percent promotional period can reduce your burden significantly.

Personal Loan for Debt Consolidation: A lower-interest personal loan to pay off high-interest credit card debt can simplify repayment and reduce overall interest cost.

Credit Counseling: Non-profit credit counseling services can negotiate on your behalf to restructure payments without the credit score damage of settlement.

Only if these options are genuinely not viable for your situation should you move toward settlement.

Real Talk: Life After Credit Card Settlement

Let me paint an honest picture of what comes after settlement.

The immediate relief is real. That constant background stress of unpayable debt lifts. The collection calls stop. You can sleep properly again.

But the financial rebuilding process takes time and discipline.

In the first year after settlement, focus on:

- Living strictly within your income

- Building an emergency fund of at least three months' expenses

- Avoiding new credit entirely

- Tracking every expense until good financial habits are deeply ingrained

In the second and third years:

- Consider a secured credit card (backed by a fixed deposit) to begin rebuilding credit history

- Make all payments on time without exception

- Gradually your CIBIL score will begin recovering

By year four or five, many people who settled credit card debt have rebuilt their credit scores to reasonable levels and can access normal financial products again.

It's not the end of your financial life. It's the end of one difficult chapter and the beginning of a more deliberate one.

Final Words

Credit card debt has a way of making people feel ashamed, trapped, and alone. If that's where you are right now, I want you to know that millions of Indians are navigating similar challenges, and there are real solutions available.

Credit card settlement in India is a legitimate, legal, and often effective way to resolve overwhelming debt when other options have been exhausted. It comes with consequences, primarily the impact on your credit score, but for many people those consequences are far more manageable than continued default and the spiral of compounding debt.

If you're seriously considering settlement and want expert guidance rather than navigating the bank negotiation process alone, The Zavo offers specialized credit card settlement services in India with a structured approach designed to get you the best possible outcome.

The most important thing is to take action. Debt doesn't resolve itself by waiting. The sooner you understand your options and make a deliberate decision, the sooner you can start moving toward financial stability.

Your debt situation is not permanent. With the right approach and the right help, there's a clear path forward.