Micro, Small, and Medium Enterprises (MSMEs) are the backbone of India's economy. They contribute significantly to employment, exports, and GDP while driving innovation across industries. However, MSME lending presents unique challenges for banks, NBFCs, fintech companies, and financial institutions due to diverse borrower profiles, cash-flow-based underwriting, regulatory compliance, and documentation complexities.

Traditional loan management methods involving spreadsheets, manual approvals, and disconnected software no longer meet the expectations of today's digital lending environment. Modern lenders require intelligent platforms capable of automating the entire loan lifecycle while reducing operational costs and improving customer experience.

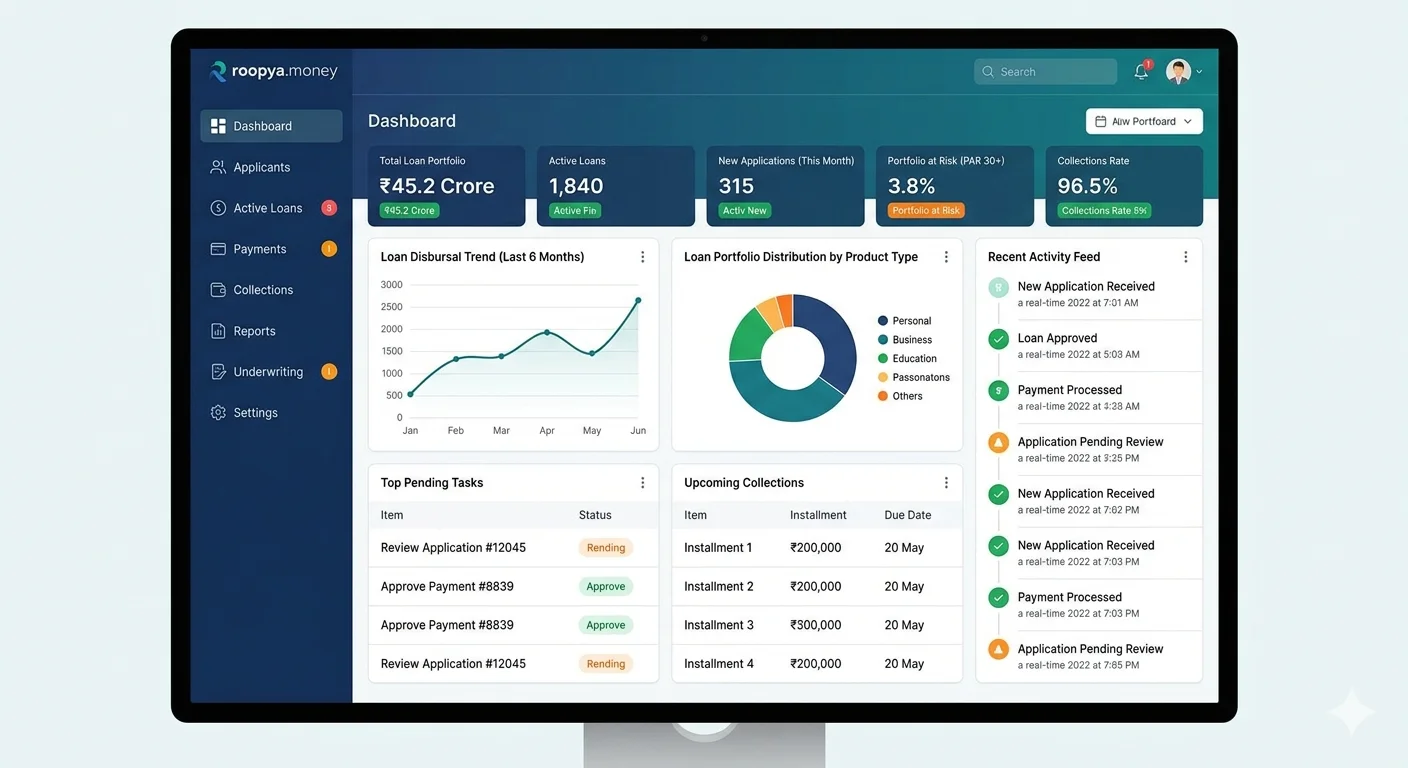

An MSME Loan Management System (LMS) is a comprehensive digital platform that manages every stage of an MSME loan—from application and underwriting to repayment, collections, reporting, and loan closure. Modern platforms like Roopya combine Loan Origination System (LOS), Loan Management System (LMS), workflow automation, AI-powered underwriting, and RBI-compliant processes into one unified lending ecosystem.

What is an MSME Loan Management System?

An MSME Loan Management System is software specifically designed to automate and streamline lending operations for MSME borrowers.

It enables financial institutions to manage:

- Loan applications

- Customer onboarding

- Digital KYC

- Credit assessment

- Document verification

- Loan approval

- Disbursement

- EMI scheduling

- Collections

- Delinquency management

- Regulatory reporting

Instead of managing multiple systems, lenders can operate from a single centralized dashboard that provides complete visibility into every loan.

Why MSME Lending Needs Specialized Software

Unlike retail lending, MSME financing requires evaluating multiple business parameters, including:

- GST Returns

- Bank Statements

- Cash Flow

- Financial Statements

- Business Vintage

- Udyam Registration

- Income Tax Returns

- Bureau Reports

- Industry Risk

- Existing Liabilities

Manual evaluation of these documents increases turnaround time and introduces operational risk.

An intelligent MSME Loan Management System automates these activities using AI, OCR, rule engines, and API integrations, enabling lenders to make faster and more accurate credit decisions.

Key Modules of an MSME Loan Management System

1. Digital Loan Origination

The journey begins with a fully digital loan application.

Features include:

- Online application forms

- Mobile-friendly onboarding

- DSA Portal

- Branch Portal

- Document Upload

- Auto Validation

- Lead Management

2. Digital KYC Verification

Modern systems integrate with:

- Aadhaar Verification

- PAN Verification

- GST APIs

- MCA Verification

- Video KYC

- DigiLocker

This eliminates manual verification while ensuring compliance.

3. Automated Credit Assessment

The system automatically collects data from multiple sources:

- Credit Bureau

- Bank Statement Analyzer

- Account Aggregator

- GST Analysis

- Financial Statement Analysis

- Business Rule Engine (BRE)

This enables instant underwriting.

4. Loan Approval Workflow

Every organization follows different approval hierarchies.

Modern LMS platforms allow configurable workflows including:

- Credit Officer

- Branch Manager

- Risk Team

- Regional Manager

- Credit Committee

- Final Approval

Role-based access improves governance and accountability.

5. Loan Disbursement

Once approved, funds are released through integrated payment gateways.

Capabilities include:

- Single Disbursement

- Partial Disbursement

- Multi-stage Disbursement

- Vendor Payments

- Escrow Payments

- Automated Notifications

6. EMI Management

The platform automatically creates:

- Amortization Schedule

- EMI Calendar

- Interest Calculation

- Penalty Interest

- Foreclosure Charges

- Part Payment Adjustments

Everything is calculated without manual intervention.

7. Collection Management

Collections are one of the most important modules.

Features include:

- SMS Reminders

- WhatsApp Alerts

- Email Notifications

- Auto Dialer Integration

- Collection Agent Assignment

- DPD Tracking

- Settlement Workflow

- Legal Recovery Process

8. Customer Self-Service Portal

Borrowers can:

- View Loan Details

- Download Statements

- Make EMI Payments

- Raise Service Requests

- Update Documents

- Track Loan Status

This reduces customer support costs significantly.

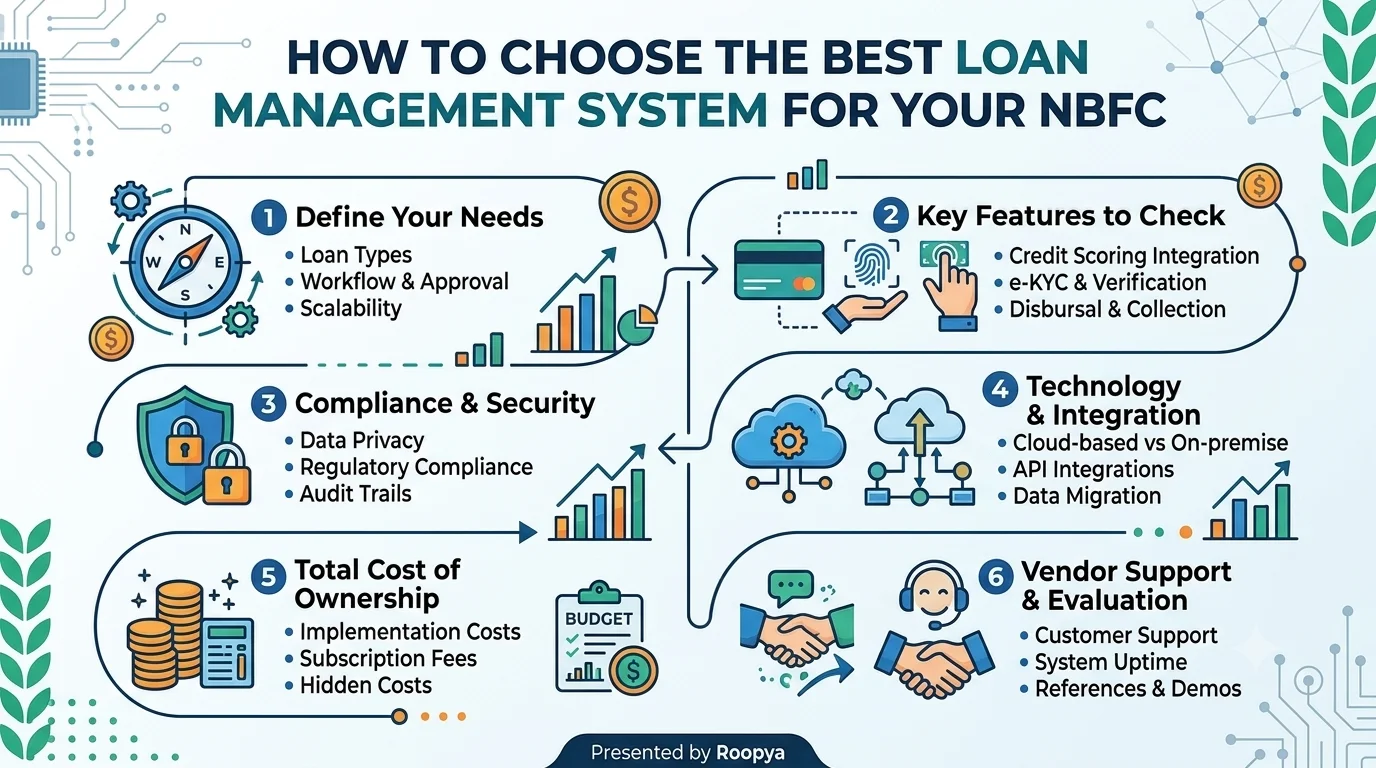

Essential Features of an MSME Loan Management System

A modern platform should include:

- End-to-End Loan Lifecycle Management

- Loan Origination System (LOS)

- Loan Management System (LMS)

- Collections Management

- Digital Onboarding

- AI-Based Credit Scoring

- OCR Document Reading

- Business Rule Engine

- Multi Bureau Integration

- RBI Compliance

- Role-Based Access

- Workflow Automation

- API Integrations

- Customer Portal

- Mobile App

- Real-Time Dashboards

- Audit Trails

- Multi Product Support

- Cloud Deployment

- Data Security

Benefits for Banks, NBFCs & Fintechs

Faster Loan Processing

Automation reduces loan approval from days to minutes.

Lower Operational Costs

Paperless workflows reduce manual work and processing expenses.

Better Customer Experience

Digital onboarding and instant status updates improve borrower satisfaction.

Reduced Credit Risk

AI-powered underwriting and automated policy checks enhance credit quality.

Regulatory Compliance

Automated audit trails and reporting help meet RBI requirements.

Improved Collections

Automated reminders and collection workflows improve recovery performance.

Portfolio Visibility

Real-time dashboards provide insights into NPAs, disbursements, overdue loans, and portfolio health.

MSME Loan Workflow

A modern lending platform follows this process:

- Customer submits online application.

- Digital KYC verification is completed.

- Documents are uploaded.

- OCR extracts information automatically.

- Credit bureau reports are fetched.

- GST and bank statements are analyzed.

- Business Rule Engine evaluates eligibility.

- Loan is approved or rejected.

- Sanction letter is generated.

- Digital agreement is signed.

- Loan is disbursed.

- EMI schedule is created.

- Automated reminders are sent.

- Collections are managed.

- Loan is closed after repayment.

Industries That Use MSME Loan Management Systems

- Banks

- NBFCs

- Fintech Companies

- Microfinance Institutions

- Co-operative Banks

- Housing Finance Companies

- Supply Chain Finance Companies

- Invoice Financing Platforms

- Equipment Finance Companies

- Commercial Vehicle Finance Companies

Why Choose Roopya for MSME Loan Management?

Roopya is a cloud-native lending platform built for modern financial institutions.

It combines:

- Loan Origination Software

- Loan Management Software

- Collections Platform

- AI-Based Underwriting

- Business Rule Engine

- OCR Document Processing

- API Marketplace

- Multi Bureau Integration

- RBI Compliance

- No-Code Configuration

With 300+ API integrations, 20+ ready-to-use loan products, AI-powered automation, and 1-day deployment, Roopya enables lenders to launch and scale MSME lending operations rapidly while minimizing manual effort.

Future of MSME Lending

The future of MSME lending is increasingly data-driven. Lenders are adopting AI, OCR, Account Aggregator integrations, and cash-flow-based underwriting to make faster decisions while expanding access to credit. Industry discussions also highlight growing reliance on digital transaction data, GST records, and alternative data sources for MSME credit assessment.

Organizations investing in intelligent loan management systems today will be better positioned to improve operational efficiency, reduce risk, and deliver a superior borrower experience.

Conclusion

An MSME Loan Management System is no longer optional for lenders aiming to remain competitive. By digitizing the complete lending lifecycle—from onboarding and underwriting to servicing and collections—financial institutions can improve efficiency, ensure compliance, and scale with confidence.

Roopya delivers an end-to-end, AI-powered, no-code platform tailored for banks, NBFCs, and fintech lenders, helping them automate MSME lending while meeting evolving regulatory and customer expectations.

Frequently Asked Questions (FAQ)

1. What is an MSME Loan Management System?

It is software that automates the complete lifecycle of MSME loans, including application, underwriting, disbursement, repayment, collections, and reporting.

2. Who should use an MSME Loan Management System?

Banks, NBFCs, fintech lenders, MFIs, cooperative banks, and other financial institutions that provide loans to MSMEs.

3. What is the difference between LOS and LMS?

A Loan Origination System (LOS) manages pre-disbursement processes such as onboarding and approval, while a Loan Management System (LMS) manages post-disbursement activities like repayment, servicing, and collections.

4. Can an MSME Loan Management System integrate with credit bureaus?

Yes. Modern platforms integrate with major credit bureaus, GST services, Aadhaar, PAN verification, payment gateways, and other third-party APIs.

5. Is Roopya's MSME Loan Management System RBI compliant?

Yes. Roopya is designed to support RBI digital lending guidelines, digital KYC, audit trails, and compliance workflows.

6. Can the system support multiple loan products?

Yes. A modern LMS can manage MSME loans alongside personal loans, business loans, vehicle loans, gold loans, and other lending products.

7. Does the system automate collections?

Yes. It supports automated reminders, DPD tracking, payment links, settlement workflows, and collection agent management.

8. Can the software be customized?

Yes. No-code platforms like Roopya allow lenders to configure workflows, approval rules, loan products, and business logic without extensive development.